GSTR-3B Filing Guide 2026 — Summary Return Made Simple

By Parul Singh, GST Practitioner · GST Returns · Updated June 2026

Table of Contents

Advertisement

What is GSTR-3B?

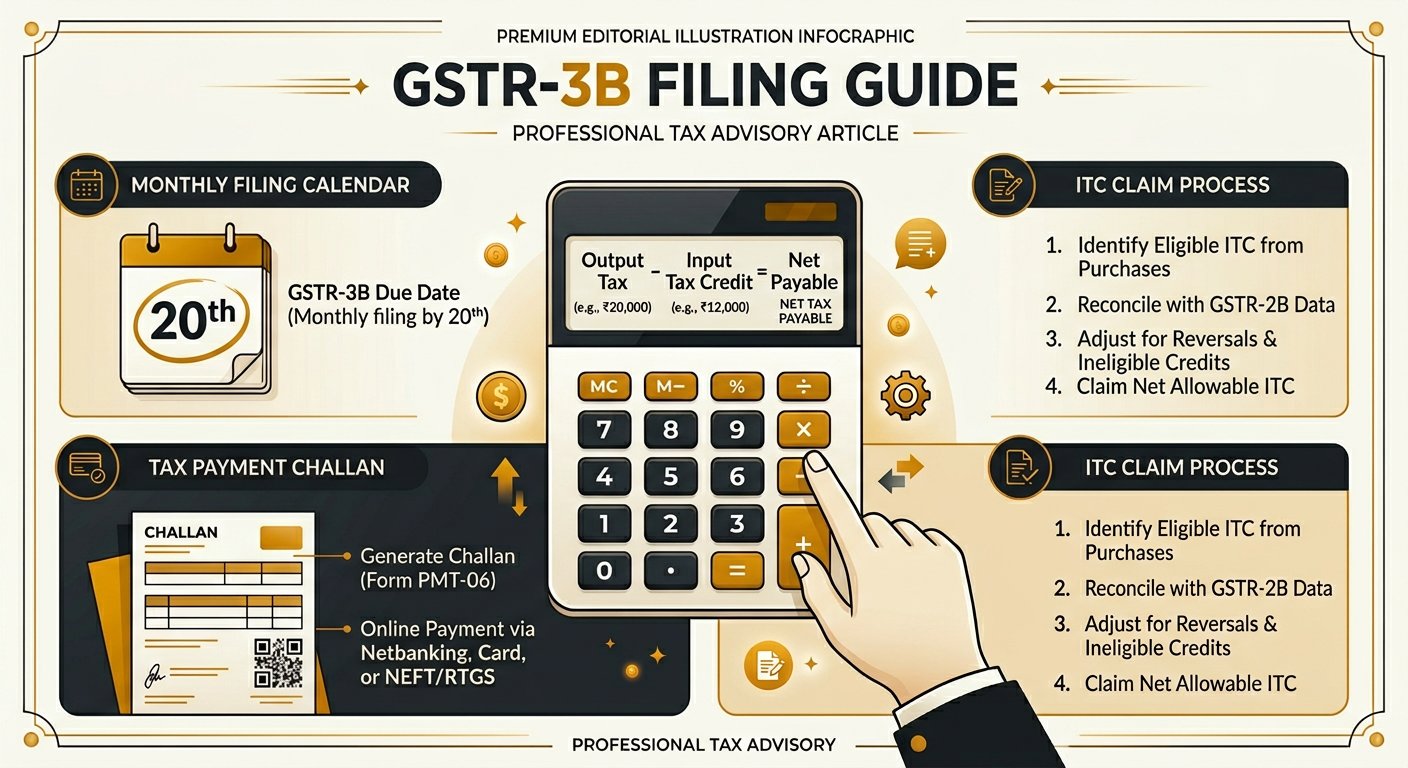

GSTR-3B is where you actually pay tax. In my practice, I have seen businesses pay ₹50,000+ in unnecessary late fees because they misunderstood this return. GSTR-3B is a summary return -- you report total outward supplies, inward supplies eligible for ITC, and pay the net tax liability.

Unlike GSTR-1 (which is invoice-level detail), GSTR-3B is a simplified self-declared return. You declare consolidated figures, not individual invoices. Think of it as: GSTR-1 tells the government WHO you sold to; GSTR-3B tells them HOW MUCH tax you owe.

Official Reference: Section 39 of the CGST Act 2017 requires filing of GSTR-3B. Rule 61 of the CGST Rules 2017 provides the form. The government introduced GSTR-3B as a simplified return through CGST (Amendment) Rules 2017, later made a permanent feature.

📍 Real Example -- Monthly Tax Payment -- Connaught Place Restaurant

A restaurant in Connaught Place with ₹15 lakh monthly sales at 5% GST:

• Outward tax: ₹75,000 (CGST ₹37,500 + SGST ₹37,500)

• Input tax on purchases: ₹30,000 (food ingredients, rent, utilities)

• Net tax payable: ₹75,000 - ₹30,000 = ₹45,000

• Must be paid by 20th of next month via GSTR-3B

• Outward tax: ₹75,000 (CGST ₹37,500 + SGST ₹37,500)

• Input tax on purchases: ₹30,000 (food ingredients, rent, utilities)

• Net tax payable: ₹75,000 - ₹30,000 = ₹45,000

• Must be paid by 20th of next month via GSTR-3B

Due Dates & Late Fees

| Taxpayer Type | Due Date |

|---|---|

| Regular monthly filers | 20th of next month |

| QRMP scheme | 25th of next month (for first 2 months), 22nd/24th after quarter |

⚠️ Common Mistake: Late fee for GSTR-3B: ₹50/day (₹20 for nil returns), capped at ₹5,000. But the REAL cost is interest under Section 50 -- 18% per annum on the unpaid tax amount from the due date until payment. For a ₹1 lakh tax liability filed 3 months late, interest alone is ₹4,500.

GSTR-3B Tables Explained

| Table | What to Report |

|---|---|

| 3.1 | Outward supplies & tax -- split by CGST, SGST, IGST |

| 3.2 | Of 3.1, supplies attracting reverse charge |

| 4 | Eligible ITC -- split by CGST, SGST, IGST |

| 5 | Exempt and nil-rated supplies |

| 6 | Payment of tax under reverse charge |

| 5.1 | Interest and late fee for previous periods |

Official Reference: Section 49 of the CGST Act 2017 prescribes the order of utilization of ITC: first set off IGST credit against IGST liability, then CGST, then SGST. The IGST credit must be fully exhausted before using CGST/SGST credit.

Claiming ITC in GSTR-3B

Table 4 of GSTR-3B is where you claim ITC. But there are strict conditions -- I see businesses making mistakes here every single month:

- ITC can only be claimed if the supplier has filed GSTR-1 (data appears in your GSTR-2A)

- ITC must be claimed in the same financial year or before September return of next year

- Blocked credits under Section 17(5) cannot be claimed -- motor vehicles, food, travel, etc.

📍 Real Example -- ITC Mismatch -- Vasant Kunj Trader

A Vasant Kunj-based electronics trader claimed ₹3.5 lakh ITC in GSTR-3B, but his GSTR-2A showed only ₹2.8 lakh (some suppliers had not filed GSTR-1). During assessment, the ₹70,000 excess ITC was disallowed with interest and penalty. Now I always advise: claim only 100% GSTR-2A matched ITC in GSTR-3B.

💡 Pro Tip from Parul: Follow this rule: Claim ITC only to the extent it appears in GSTR-2A. For the unmatched portion, follow up with suppliers and claim in subsequent months. This avoids interest and penalty on excess ITC claims.

Step-by-Step Filing Process

- Login to gst.gov.in → Returns Dashboard

- Select the return period

- Click "Prepare Online" for GSTR-3B

- Fill Table 3.1: Enter outward supply details (auto-populated from GSTR-1)

- Fill Table 4: Enter eligible ITC (cross-check with GSTR-2A)

- Review the tax liability calculation

- Create challan for any net tax payable (use DRC-03 for interest/penalty)

- Pay tax via net banking/neft/upi

- File GSTR-3B using DSC or EVC

Common Mistakes in GSTR-3B

- Claiming ITC without GSTR-2A match -- leads to demand notice

- Wrong order of ITC utilization -- IGST must be used first

- Not reporting reverse charge liability -- hidden cost that surfaces during audit

- Filing nil return when there are purchases -- loses ITC permanently

- Not paying interest on delayed filing -- interest under Section 50 is mandatory

⚠️ Common Mistake: The most dangerous mistake: claiming ITC in GSTR-3B but the supplier has not filed their GSTR-1. The IT department's automated system flags this, and you will receive a notice under Section 73 or 74 to reverse the ITC with interest and penalty. Always reconcile before filing.

💡 Pro Tip from Parul: I provide monthly GSTR-3B filing service with ITC reconciliation for ₹1,499/month. Never miss a deadline or lose ITC. Call/WhatsApp: +91 95401 04776

Advertisement

Frequently Asked Questions

What is the difference between GSTR-1 and GSTR-3B?

GSTR-1 reports your sales (outward supplies) invoice by invoice. GSTR-3B is a summary return where you report total sales, claim ITC, and pay net tax. GSTR-1 data auto-populates GSTR-2A of your buyers; GSTR-3B is your actual tax payment return.

Can I file GSTR-3B before GSTR-1?

Yes, technically you can. However, I recommend filing GSTR-1 first because the outward supply data from GSTR-1 auto-populates Table 3.1 of GSTR-3B, reducing errors. Many Delhi businesses file GSTR-1 by 10th and GSTR-3B by 18th to stay ahead of deadlines.

What if I make a mistake in GSTR-3B?

Unlike GSTR-1, there is no amendment facility for GSTR-3B. You can only correct errors through subsequent period returns. For excess ITC claimed, you must reverse it in the next period. For short reporting, you can add it in the next period's return.

Advertisement