Input Tax Credit saved my clients a combined ₹12 crore last year. But I also see businesses lose ITC worth lakhs because they do not follow Section 16(2) conditions correctly. ITC is the credit you get for the GST paid on your business purchases — it reduces your output tax liability, so you pay only the net tax on your value addition.

ITC — claim credit for GST paid on business purchases

Official Reference: Section 16 of the CGST Act 2017 defines ITC and its conditions. Section 17 deals with apportionment of credit and blocked credits. Section 18 covers ITC in special circumstances like new registration, change of regime, etc.

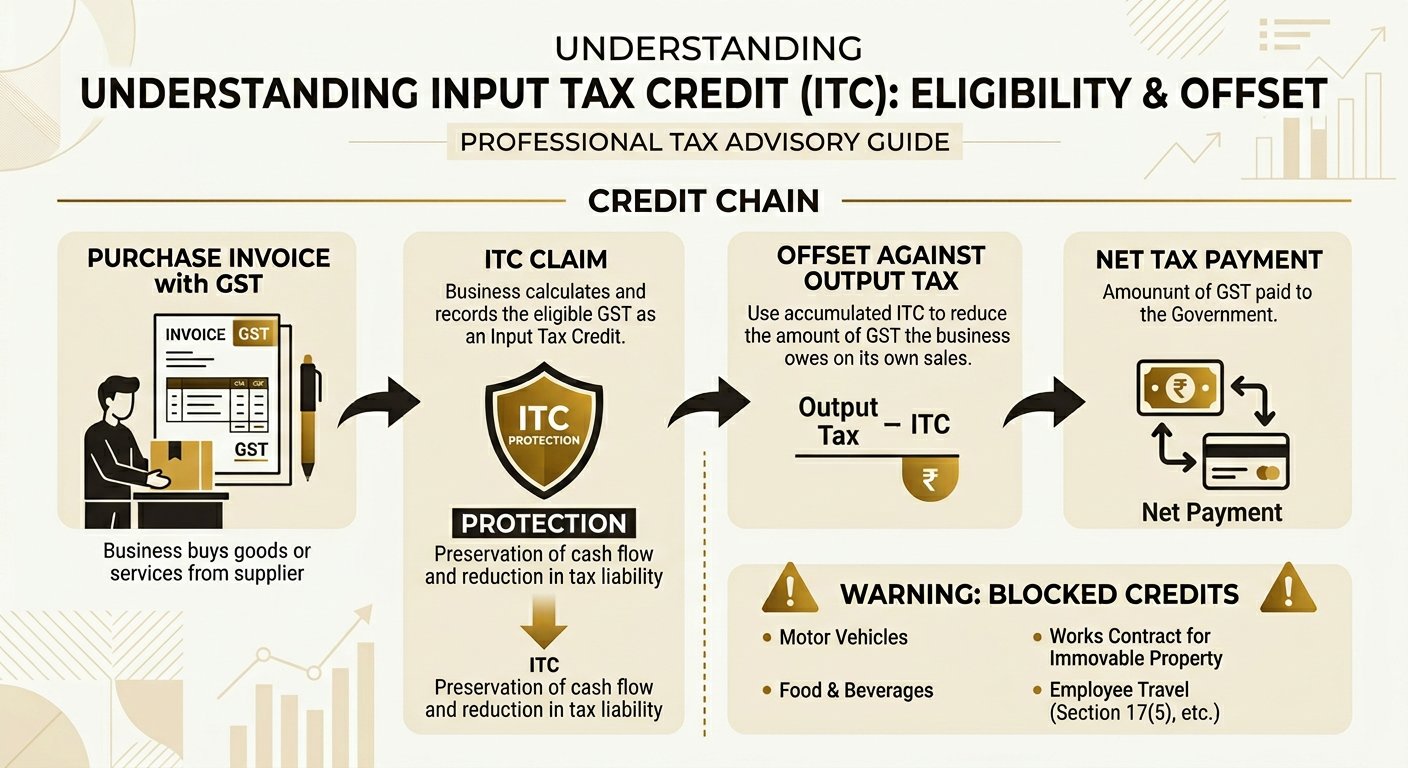

ITC is the backbone of the GST system. Without it, GST becomes just another cascading tax. The entire chain works because each person can claim credit for tax paid to their supplier:

Output Tax - Input Tax Credit = Net Tax Payable

📍 Real Example — Karol Bagh Electronics Dealer

A dealer in Karol Bagh purchases mobile phones worth ₹10,00,000 + ₹1,80,000 GST (18%). He sells them for ₹12,00,000 + ₹2,16,000 GST. • Output tax: ₹2,16,000 • Input tax credit: ₹1,80,000 • Net GST payable: ₹2,16,000 - ₹1,80,000 = ₹36,000 • He pays tax only on his ₹2,00,000 value addition

Eligibility Conditions for ITC

Section 16(2) lays down 4 conditions that must ALL be satisfied. Missing even one means no ITC. I see violations of these conditions every single day:

Possession of tax invoice — you must have a valid GST invoice from the supplier

Receipt of goods or services — goods must be delivered to you (last instalment for split delivery)

Furnishing of return — you must have filed GSTR-3B for the period

Supplier has filed GSTR-1 — the supply must appear in your GSTR-2A (added by amendment)

Payment to supplier — you must have paid the supplier within 180 days (Section 16(2)(d))

Official Reference: Section 16(2)(c) as amended by Section 109 of Finance Act 2022 makes ITC available only if the supply has been furnished by the supplier in their GSTR-1 and appears in the recipient's GSTR-2A. This is the most critical condition for ITC eligibility.

📍 Real Example — Missed Payment — Kirti Nagar Furniture Maker

A furniture manufacturer in Kirti Nagar bought ₹5 lakh of wood with ₹90,000 GST. But he paid the supplier after 210 days (beyond the 180-day limit). Under Section 16(2)(d), he had to reverse the ₹90,000 ITC and add it to his output tax. He could re-claim it only after making the payment. This cost him interest of ₹2,700 on the reversed amount.

Blocked Credits — Section 17(5)

This is where I see the most confusion. Not all ITC is claimable, even if you have a valid invoice. Section 17(5) blocks ITC on specific items:

Motor vehicles — except for further supply, transport, or driving training (₹25 lakh seating capacity)

Food, beverages, outdoor catering — unless you are in the business of supplying these

Travel, tour, and hotel — unless you are a travel agent

Health, fitness, cosmetics, salon — unless you supply these

Membership fees, club, health/fitness center

Construction of immovable property — unless you are a builder

Goods/services for personal use

⚠️ Common Mistake: The most common blocked credit mistake: businesses claiming ITC on office car purchase. A ₹10 lakh car attracts ₹1.5 lakh GST, and businesses try to claim it as ITC. Unless you are in the transport business, this ITC is blocked under Section 17(5)(a). The department catches this during GSTR-9 audit.

How to Claim ITC

Verify supplier's GSTR-1 filing — check GSTR-2A before claiming

Claim in GSTR-3B — Table 4 (eligible ITC)

Follow the utilization order — IGST credit first, then CGST, then SGST

Reconcile monthly — match GSTR-2A with purchase register

Claim within deadline — by September return of next FY or date of annual return, whichever is earlier

ITC Reversal

Sometimes you must reverse ITC already claimed. The most common reasons:

Rule 42/43: ITC on common inputs used for both taxable and exempt supplies — proportional reversal

Section 16(2)(d): Payment to supplier not made within 180 days

Rule 37: Supplier has not paid tax (GSTR-2A mismatch)

📍 Real Example — Proportional Reversal — South Extension Textile Business

A textile business in South Extension deals in both taxable (18% GST) and exempt (handloom) items. Total ITC for the month: ₹2,40,000. Taxable turnover: ₹18 lakh, Exempt turnover: ₹6 lakh. Common ITC to reverse = ₹2,40,000 × (6/24) = ₹60,000. Net claimable ITC: ₹1,80,000. Under Rule 42, this reversal must be done monthly in GSTR-3B.

💡 Pro Tip from Parul: Maintain a separate ITC register. Every month, track: (1) Total ITC per purchase register, (2) ITC available in GSTR-2A, (3) ITC actually claimed in GSTR-3B. The gap between (2) and (3) is your unmatched ITC — follow up with those suppliers immediately.

Common ITC Mistakes I See

Claiming without GSTR-2A match — #1 cause of demand notices

Not reversing blocked credits — office car, staff canteen, guest house

Missing the 180-day payment deadline — set up payment reminders

Not doing Rule 42/43 reversal — for businesses with exempt supplies

Claiming ITC on personal expenses — clear separation of business vs personal

💡 Pro Tip from Parul: I offer monthly ITC reconciliation as part of my GST return filing service. We ensure you claim every rupee you are entitled to — and nothing you are not. Starting at ₹1,499/month. Call/WhatsApp: +91 95401 04776

Advertisement

Frequently Asked Questions

Can I claim ITC if my supplier has not filed GSTR-1?

No. As per Section 16(2)(c), ITC is available only if the supply appears in your GSTR-2A. If the supplier has not filed GSTR-1, you cannot claim ITC. Follow up with the supplier or find an alternative supplier who files on time.

What is the time limit for claiming ITC?

ITC must be claimed by the due date of filing the return for September of the following financial year, or the date of filing the annual return, whichever is earlier. For FY 2025-26, the last date to claim ITC would be 20th October 2026.

Can ITC be refunded?

Yes, ITC can be refunded in specific cases: exporters (zero-rated supplies), inverted duty structure (where input tax rate exceeds output tax rate), and accumulated credit due to inverted rate structure. File refund application under Section 54.

Advertisement

Need Help with This?

Get expert assistance from a GST Practitioner with 15+ years experience. Fast, affordable, and reliable.