What is GST? A Complete Guide for Indian Businesses in 2026

Table of Contents

What is GST?

In my 15+ years as a GST Practitioner in Karol Bagh, New Delhi, I have helped over 1,500 businesses understand and comply with GST. Before 1st July 2017, India had a chaotic indirect tax system — VAT, service tax, central excise, octroi, entry tax, and luxury tax were all levied at different stages by different authorities. A single product could be taxed 5+ times before reaching the consumer, creating what we call the cascading effect or "tax on tax."

Goods and Services Tax (GST) changed all of that. Launched on 1 July 2017 under the Constitution (101st Amendment) Act, 2016, GST is a destination-based, multi-stage tax levied on every value addition. It replaced 17 central and state taxes and 23 cesses with a single, unified tax structure.

As of 2026, India's GST system has matured significantly with monthly collections consistently exceeding ₹1.94 lakh crore. The GST Council, chaired by the Union Finance Minister, has made over 50 rate changes since inception, continually refining the system.

Types of GST in India

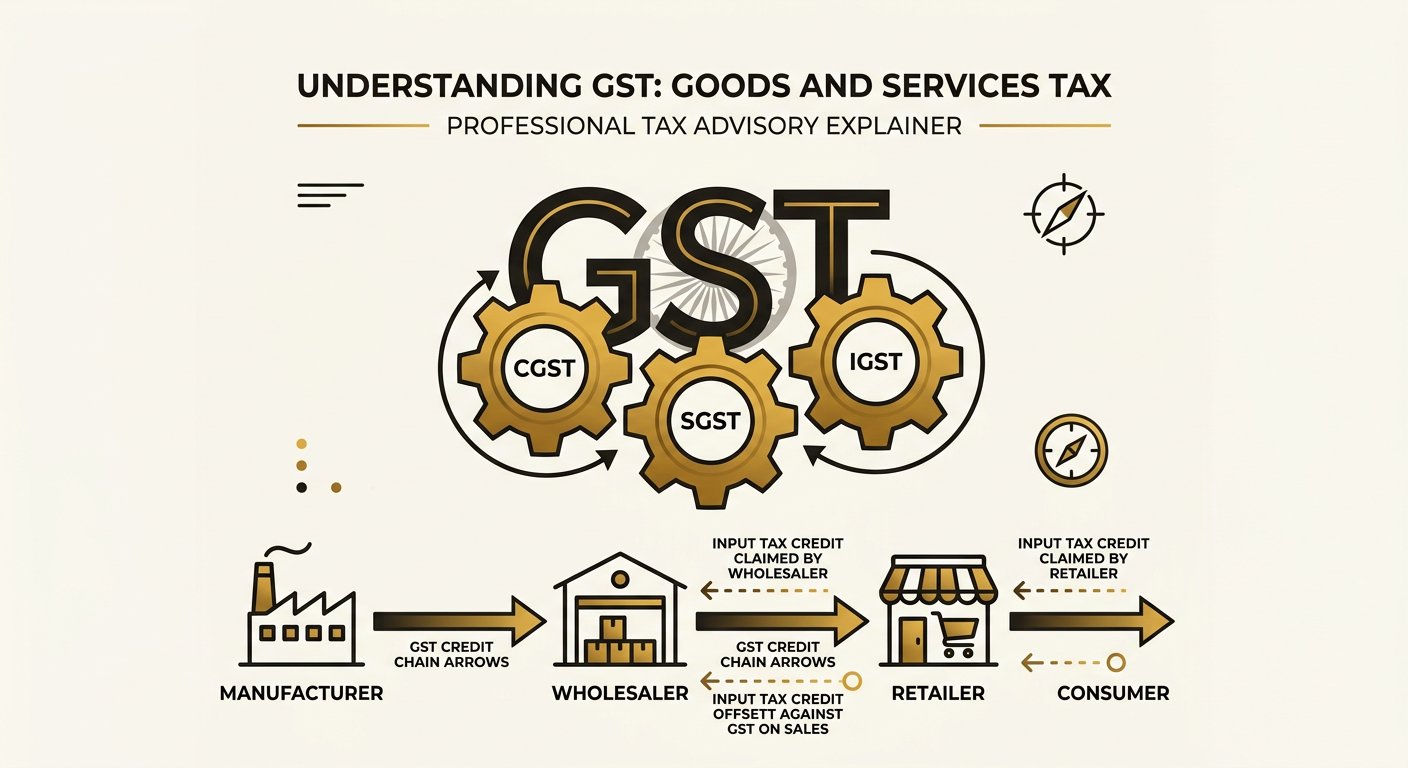

GST in India follows a dual model — both the Centre and States levy it simultaneously on the same transaction. Understanding the types is critical for any business, whether you are a small trader in Chandni Chowk or a large manufacturer in Okhla.

| Type | Full Form | Levied By | When Applicable |

|---|---|---|---|

| CGST | Central GST | Central Government | Intra-state supply |

| SGST | State GST | State Government | Intra-state supply |

| IGST | Integrated GST | Central Government | Inter-state supply & imports |

| UTGST | Union Territory GST | Union Territory | Intra-UT supply |

• CGST @ 9% = ₹900

• SGST @ 9% = ₹900

• Total GST = ₹1,800

Inter-state: Same dealer sells to Mumbai buyer:

• IGST @ 18% = ₹1,800 (single component)

GST Registration Thresholds

Not every business needs to register for GST. The thresholds vary by state category, type of supply, and business type. As a GST consultant in Delhi, I get 20+ calls every week asking Do I need GST registration? — here is the definitive answer.

| Category | Threshold (Annual Turnover) |

|---|---|

| Normal category states (goods) | ₹40 lakh |

| Special category states (goods) | ₹20 lakh |

| Service providers | ₹20 lakh (₹10 lakh for special states) |

| E-commerce operators | No threshold — must register |

| Inter-state suppliers | ₹20 lakh |

| Input Service Distributors | Mandatory regardless of turnover |

How GST Works — The Credit Chain

The real power of GST lies in the Input Tax Credit (ITC) mechanism. Under the old regime, you paid tax on your purchases but could not claim credit across different tax types. Under GST, every person in the supply chain can claim credit for the GST paid on their purchases — creating a seamless credit chain.

Here is how the credit chain works at each stage:

- Manufacturer buys raw materials for ₹100 + ₹18 GST. Sells finished goods for ₹200 + ₹36 GST. Pays ₹36 - ₹18 = ₹18 net GST.

- Wholesaler buys for ₹200 + ₹36 GST. Sells for ₹300 + ₹54 GST. Pays ₹54 - ₹36 = ₹18 net GST.

- Retailer buys for ₹300 + ₹54 GST. Sells for ₹400 + ₹72 GST. Pays ₹72 - ₹54 = ₹18 net GST.

Total tax collected: ₹72 on a value addition of ₹400 — exactly 18% of the final price, with no cascading. Each person pays only the tax on their value addition.

Benefits of GST

Despite initial implementation challenges, GST has delivered significant benefits to the Indian economy and businesses:

- One Nation, One Tax: Unified tax structure across India — no more navigating different state VAT laws

- Elimination of cascading: ITC ensures tax is only on value addition, reducing effective tax burden by 25-30% on most goods

- Simplified compliance: Single online portal (gst.gov.in) for everything — registration, returns, refunds

- Lower overall tax burden: Most essential goods are cheaper than pre-GST due to lower rates and credit mechanism

- Logistics efficiency: No border check-posts, faster movement of goods — a truck from Delhi to Mumbai now takes 30% less time

- Formal economy growth: GST registration has brought 1.4+ crore businesses into the formal economy

Basic GST Compliance Requirements

Running a business in Delhi without GST compliance is like driving without a license — you will get caught eventually. Here are the basics every registered taxpayer must follow:

- GST Registration: Within 30 days of crossing threshold (Section 22)

- GSTR-1: Monthly/quarterly filing of outward supplies by 11th of next month

- GSTR-3B: Monthly summary return with tax payment by 20th

- E-way Bill: For movement of goods above ₹50,000 (Rule 138)

- E-invoice: Mandatory for businesses above ₹5 crore turnover

- Annual Return (GSTR-9): Yearly reconciliation by 31st December

Common GST Mistakes I See in Delhi

In my practice, I see the same mistakes repeated across businesses — from traders in Gandhi Nagar to startups in Nehru Place:

- Not registering when required — especially freelancers doing inter-state work

- Wrong type of GST charged — CGST+SGST on inter-state sales instead of IGST

- Not claiming ITC — many small businesses do not even know they can claim credit

- Late filing — ₹50/day late fee adds up quickly; I have seen businesses owe ₹25,000+ in just late fees

- Incorrect HSN codes — wrong classification means wrong rate and potential demand notice